What’s Happening in the Explosive 10-Minute Delivery Space and What’s Next?

Ultra-fast delivery startups have emerged as key investment trends among today’s venture capitalists. Startups promise to deliver goods to the consumer in less than 20 minutes. Alongside the pandemic-fueled acceleration of Ecommerce adoption, the rapid DtC Ecomm space has become fertile ground for institutional investment.

The Perfect Storm

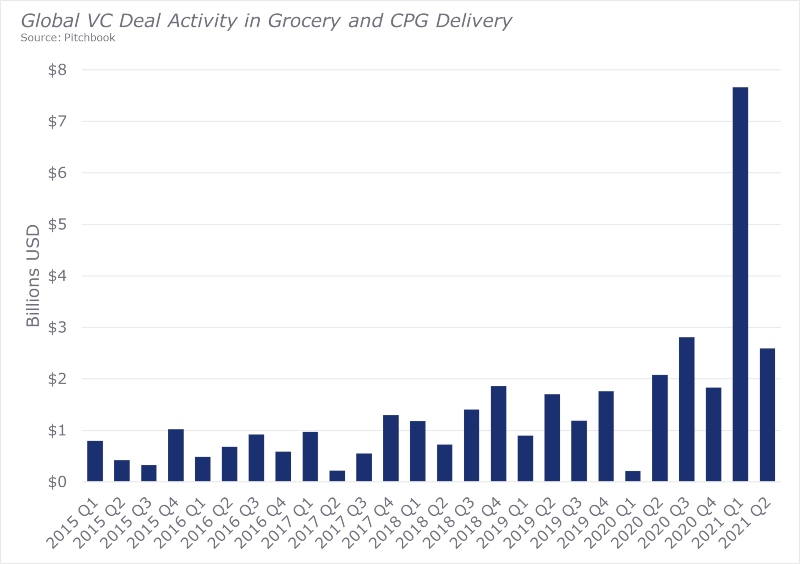

Venture-backed grocery companies have reportedly raised over $7 billion USD in funding throughout 2020 and eclipsed that figure in just the first quarter of 2021. Two of the more established players in this space, Instacart and GoPuff, observed latest funding rounds that valued each at an eye-popping $39B and $15B, respectively. Plus, the venture-backed deluge of new entrants has not slowed down, with players like Jokr and Gorillas amassing 9-10 figures in funding in mere months.

The Latest Players are Differentiated by Extreme Speed

The biggest differentiator touted by these startups is the extremely short window they can achieve between placing an order and completing delivery. The entire business model is optimized for speed, resulting in major departures from the operational, fulfillment, and inventory norms set by the (now considered) legacy players like Instacart, DoorDash, and Peapod. The newest upstarts also target a different consumption occasion from established players.

Snapshot of Notable Delivery Startups Making Inroads in the US:

Established DtC ecommerce players like Peapod, DoorDash, and Instacart specialize in picking and delivery while relying on retailers’ inventory and physical assets. The latest generation of startups, meanwhile, take on much more capital risk in exchange for a faster delivery time and greater control over the customer experience.

There are 3 notable shifts in the business model:

- They own the inventory: Today’s emerging providers own their inventory rather than relying on a partner’s pre-selected assortment. This gives them control over the assortment and margins but creates capital risks and requirements as well as supply chain sophistication to be profitable.

- They take on real estate liabilities: The secret to their speed is having a network of highly efficient dark store or micro-fulfillment centers (MFC) located close to the end-consumer where goods can be picked 5-10x more efficiently than from store shelves and delivered rapidly. While efficient, these facilities require significant CapEx to build in addition to real estate costs (our recent whitepaper outlining these next-gen fulfillment models is available for download on our site).

- They have a higher labor commitment: Many of these providers rely, at least in part, on a workforce of traditional employees rather than flexible and inexpensive gig-economy contractors. Dark store models require highly trained employees to do the picking and even highly automated MFCs require operators to run. Additionally, with the promise of rapid 10-20 minute delivery, these providers may need to employ at least some traditional employees as drivers to ensure they can consistently meet consumer demand rather than relying on the self-selected schedules of gig-economy contractors.

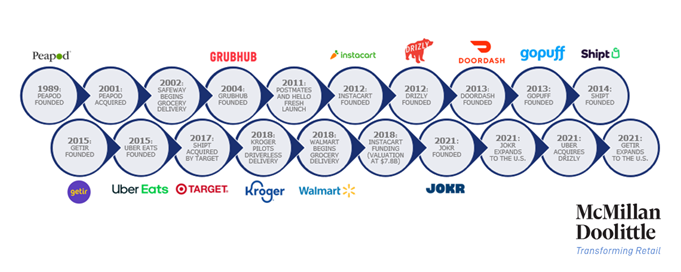

A Timeline of DtC Ecommerce Delivery in the US:

Source: McMillanDoolittle Research

Who are the New Entrants Putting at Risk?

The first question a retailer might ask is whose market share these well-funded startups are taking. The key is understanding the consumption occasions that prompt consumers to turn to these providers. Based on the assortment of goods these providers carry and their 10-minute differentiator, their most relevant consumption occasion is for “need it now” situations rather than stock-up grocery trips or meal occasions.

Based on their fulfillment model, these providers need to carry a very compact assortment of goods (less than 7K SKUs) and are likely to gravitate toward non-perishable and/or fast-turning goods to optimize supply chain efficiency; in other words, their logical focus categories will likely be convenience, CPG, alcohol, basic grocery and personal care, and/or inexpensive consumer tech (e.g., phone chargers or tobacco vapes). These assortment constraints and their speed imply they will mainly be stealing share from convenience, liquor, and drug stores, but impacting grocery and mass retailers to a much lesser degree.

What Justifies Outsized Investment in the Space?

Another question might be on the explosion of this startup space: what is encouraging all the VC activity, and why have so many different providers emerged? This may have more to do with the venture capital model rather than market demand: the goal of a VC is not necessarily to build a mature business but rather to execute a successful exit by achieving a good ROI on their initial investment.

McMillanDoolittle Point of View

Our perspective is that few of these startups will be able to become profitable, mature standalone businesses. They face some steep hurdles, including:

- Their assortment and fulfillment models limit the consumption occasions where these providers will be relevant, limiting share of wallet with consumers

- Their business model is very capital-intensive meaning they need significant scale to offset costs and break even

- They sell low-margin categories with high demand elasticity, so they face significant margin challenges. Expanding to adjacent categories like fresh grocery is a major logistical undertaking.

- They have high skilled-labor requirements in an economy where these are in high demand and short supply

- They face dozens of similar competitors in their space, and large retailers or established delivery providers with deep pockets could launch competing services with relative ease (in fact both Instacart and UberEats are piloting 15-minute deliveries in specific markets)

- The daily improvements in predictive analytics and in automated vehicles may enable the creation of alternative business models to meet this same consumption occasion in the near future

- For their business model to be profitable, they require a high density of customers in their delivery radii. While this may work in the population-dense geography of Western Europe where many of these startups began, the low population density of North America as a whole presents expansion challenges beyond major cities.

The size of the prize on low-margin product categories with an expensive fulfillment model is limited, but the exit opportunities for VC firms are very attractive:

- Many VC exits occur when the fund’s equity is liquidated during M&A activity, with the VC aiming to turn a big profit. In a competitive space with dozens of entrants, we will likely see consolidation among these emerging players through both mergers and acquisitions.

- Additionally, competitors that can differentiate through demonstrated growth or by developing valuable customer or IP assets will be attractive acquisition targets for both large retailers like Walmart or 7-Eleven, and tech providers like Uber, Instacart, or Amazon.

- Competitors that can develop alternative revenue streams will also become attractive acquisition targets or become successful companies in a less challenging arena than retail. For example, these providers can use their marketplace as a paid ad platform for CPG companies, or they could monetize the valuable customer data they are harvesting. Additionally, they could succeed by developing impactful IP assets (e.g. a game-changing fulfillment optimization platform) and selling them profitably as a SaaS provider, much like Amazon is doing with their Just Walk Out technology.

In a burgeoning industry with dozens of emerging players, big VC bets, and eyes on a rapid exit horizon, the only constant will be change. Follow McMillanDoolittle for ongoing coverage and commentary on this and other trends changing the face of retail. You can also contact me with any thoughts or questions.

No Comments