An Uncertain Future for GoPuff, Getir, & Other Rapid-Delivery Providers

Back when 10-minute delivery startups were surging, we predicted these “rapid delivery” players would struggle or even perish unless they diversified their revenue streams or joined a larger ecosystem. Today’s economic conditions are exacerbating their challenges. Read on for our take on the current landscape in rapid delivery.

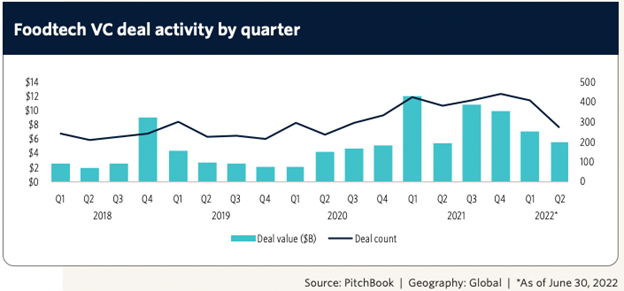

Following initial VC-backed growth in 2020 and 2021, many rapid-delivery startups have had to scale back in recent months. Gorillas, Getir, and Jokr – each valued at over $1B last year – have all announced cuts to their operations and workforces, with Jokr slashing their US operations completely. Even American market pioneer GoPuff has reportedly undergone real estate closures and staff downsizing this year.

A Business Model Plagued by Trade-offs

While the entire paid delivery space is threatened by economic pressures, this class of provider is at particular risk as a standalone business model due to two major trade-offs they made in order to achieve unparalleled speed. The first of these challenges is the undifferentiated assortments they carry, which limits their ability to stand out from competitive delivery offerings. The second and arguably bigger problem is their high fixed cost burdens that is less nimble to changes in demand relative to retailer-owned and gig-economy-based delivery competitors. We break down how these two issues are plaguing rapid delivery and putting the future of the 10-minute delivery model in peril.

Not the Best Choice for Most Purchase Occasions

Successful retail strategies are centered on the ability to resolve a customer need better than any other company – and to do so with enough scale to produce a viable business. The ability to deliver a small assortment of common types of consumer packaged goods (CPG) or alcoholic beverages in 10 minutes solves a problem with limited applicability for the consumer:

- If a consumer wants common CPG or alcoholic beverages but is not in a hurry, these providers are not differentiated from a slower delivery model or a nearby retailer

- If a consumer wants anything other than an essential product, these providers won’t be an option due to their limited assortments

- The only relevant use case for rapid delivery is when a consumer needs one of a limited (7,000 or fewer) number of SKUs and needs it immediately. Otherwise, these types of providers are no better than anyone else.

Unless rapid-delivery providers can find a way to grow their ceiling of potential transactions, they will be restricted in their growth and ability to become profitable.

A Long-Horizon Business Model Threatened by Short-Horizon Conditions

To achieve their logistical speed, rapid-delivery providers require significant capital up-front for real estate, advanced picking hardware and software, fleets, labor, and inventory. They also require a high sales volume to overcome their fixed costs and thin grocery margins, creating a long road to profitability. This poses 2 obvious problems in today’s environment:

- A high fixed-cost model is not adaptable to changes in demand. If sales volume dips with recession-wary consumers, they will have a hard time adjusting costs and keeping a healthy balance sheet.

- To grow despite high costs, these companies have been heavily reliant on venture capital funding. VCs appear increasingly risk-adverse and cautious with their investments in an increasingly uncertain economic environment. Reduced funding limits these providers’ ability to invest in growth, creating a vicious cycle where limited growth numbers then turn off potential investors and lower these companies’ valuations.

Meanwhile, these startups’ competitors are better poised to weather short-term hardship. Gig-economy-based competitors like Instacart are nimbler with their cost-structure, only paying for labor and inventory when an order has been placed. Retailer-owned delivery options like Amazon Fresh or Target’s Shipt have the backing of major corporations who can absorb short-term hits or decide to take small losses if it means gaining market share or share of wallet.

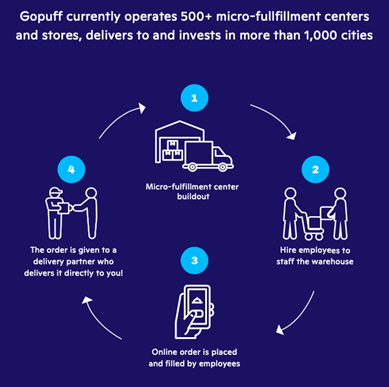

Fast but Capital-Intensive: Rapid delivery providers invest heavily in real estate, technology, logistics, staff, and inventory to achieve their 10-minute speed. (Image via GoPuff).

At this stage, rapid-delivery providers will have to operate in the small number of highly populated geographies with potential for order density. We imagine many of the most recent entrants to this space – who created parallel delivery networks to serve many of the same markets – will quickly become redundant and unsustainable as long as economic uncertainty continues.

What Can Incumbents Do to Survive?

To survive and thrive, 10-minute delivery startups must understand what other types of consumer or B2B needs they can solve better than any other type of company – and then aggressively pursue those opportunities as their primary business.

This could mean new or different product assortments or geographies. It could mean right-sizing or redeploying assets to fit this mission. It will likely require market research and targeted marketing efforts. They may also find that their innovative fulfillment model is more likely to succeed as just one of several tools a provider or retailer can employ while meeting a wide range of customer needs.

At McMillanDoolittle, we help companies develop successful growth strategies by understanding who to target, how to target them, and how to align their business model with this mission. If this sounds like the right approach for your business, get in touch with me to talk more.

No Comments