Saks’ Ecommerce Spin-off: Shrewd Move or Faustian Bargain?

Ailing US department stores are increasingly pressured to spin off their Ecommerce operations. We share our thoughts on whether these moves make for a clever strategy or merely offer a last resort.

The retail world has been abuzz with Ecommerce spin-offs, beginning with Saks Fifth Avenue’s 2021 break up and recent activist pressure calling for similar moves for Macy’s and Kohl’s. While splitting a retailer’s Ecommerce and brick-and-mortar businesses into separate entities may make logical sense as a financial maneuver, it is also likely to create major hurdles in delivering the seamless omnichannel experience today’s consumers increasingly expect.

Spinning off Ecommerce Operations Can “Unlock Value” for Shareholders

In the current business environment, tech and Ecommerce companies trade at much higher relative valuations (2-3x higher based on sales) than traditional retailers. The driving concept behind splitting digital and physical business units is to unlock the value for the high-growth digital side of the business through a higher valuation.

At least in the short term, this strategy to raise capital by separating the high-growth areas of the company from the legacy units seems to be working for Saks stakeholders: During early 2020, Saks was taken private at a $1.5B valuation. During a VC funding round last March, the Ecommerce side of the combined business was alone valued at $2B. Now the standalone Ecommerce entity is reportedly targeting a $6B valuation as it prepares for a 2022 IPO (Per WSJ).

This is all independent of the Saks Off Fifth discount vertical, which underwent a parallel Ecommerce and brick-and-mortar split. Both the Saks and Saks Off Fifth brick-and-mortar entities are likely to remain private under the HBC parent company.

Splits Also Offer an Opportunity to Revamp the Organization and Brand

Aside from this influx of funding, the separate Ecomm entity can now more effectively revamp its culture and image: as an organization, the Ecomm entity can now fully embrace a high-growth, tech-focused culture and image, potentially becoming a more exciting destination for top talent and fostering organizational agility. The split is also an opportunity for rebranding efforts, exemplified by Off Fifth’s digital-led rebrand to appeal to younger consumers.

The Saks agreement also sought to insulate its IP and branding rights in what it sees as the “healthier” business, granting these rights to the Ecomm entity, meaning they will remain protected if the brick-and-mortar entity enters bankruptcy or restructuring.

Emergency Maneuvers Offer a Last Resort

Spinning off the Ecommerce business is not a move that should be taken lightly. It strikes at the heart of the careful balance leaders of public companies often must weigh, between maximizing short-term shareholder value and optimizing the customer experience for the long haul.

For years, the prevailing ethos in retail has been to fully harmonize the online and offline channels to create a cohesive omnichannel customer experience, and this has never been more relevant than for today’s tech-savvy consumer. Beyond providing a channel-agnostic experience, dynamic retailers utilize their digital and physical channel presence synergistically to build their brand’s reach and equity.

Saks’ stakeholders have attempted to get the best of both worlds, crafting over 300 transition and operating provisions to keep the customer experience unchanged while managing the split behind the scenes. Maintaining a cohesive customer experience through agreements, guidelines, and the threat of legal action is not impossible (international franchisors like McDonald’s do it at mass scale extremely well), but it makes collaboration that much more challenging, especially when each business unit now answers to different investors and has differing business objectives.

Do Other Options Exist?

Macy’s and Kohl’s recent resistance to this sort of split illustrates the risk retail leaders ascribe to such a dramatic move. At the end of the day, suggestions to split business units are precipitated by a lack of investor confidence in the value of brick-and-mortar. However, giving up on brick-and-mortar may hurt the overall brand and have downstream impacts on the dot-com entity.

Before embarking on a split, retail leaders and investors should focus on accurately measuring the accretive value of physical stores and maximizing it.

- Adequately recognize the impact of stores: Stores present value above and beyond store transactions. They can serve as a showroom for products later bought online, as a pickup point for omnichannel orders, as a distribution point for product deliveries, and perhaps most importantly as a marketing tool to build brand awareness and customer connection. Despite the advancements in VR and AR, there is no existing substitute to an immersive and compelling physical shopping experience when it comes to building customer connection and lifetime value. Financial leaders and investors have a prevailing motive to accurately model and measure these added benefits of brick-and-mortar stores.

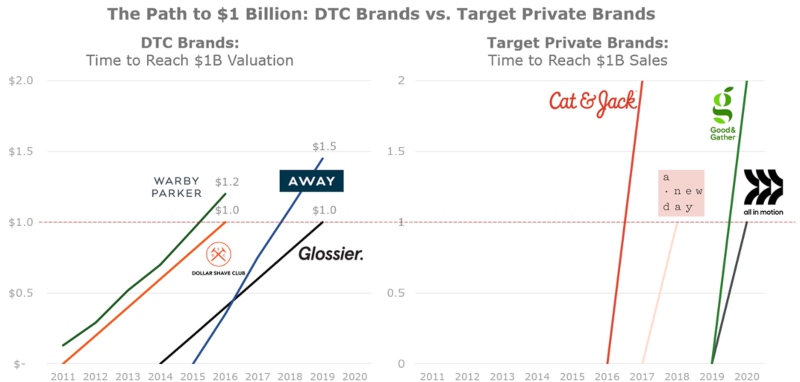

Ecommerce-only brands grow more slowly than those supported with strong store placement. They also tend to struggle with profitability.

Source: Refinery29, Chart Mogul, Business Insider, CNBC, Pitchbook

- Maximize the performance of retail space: Larger-format retail stores struggle with floorspace efficiency. Retailers should seek to make the most of their physical assets through the traditional set of tools to boost traffic and conversion, and to increase trade-up and attachment rate. They can also employ more creative solutions like shop-in-shops or joint ventures to better utilize their retail space, as Kohl’s has begun to do with Sephora and Amazon. Maximizing the utility of physical assets requires discipline and sometimes difficult decisions when it comes to right-sizing store portfolios and deploying the right store formats.

Both these steps take time, and even if completed may not be enough to satisfy activist investors. In the meantime, we will continue to watch the Saks Fifth Avenue experiment and see if the short-term financial upside is worth the long-term risks to the customer experience. To stay up to date on our latest retail insights, follow us on LinkedIn. To continue the conversation, simply Contact Me.

No Comments